Instacart Shares Fall As Investors Shy Away From Slow-Growing Grocery

Instacart’s strong Q4 and full-year performance was not enough to soothe investor and analyst fears about the slow growth set to capture the grocery industry in 2025 as shares were down 9.66% to $44.04 per share today in mid-morning trading.

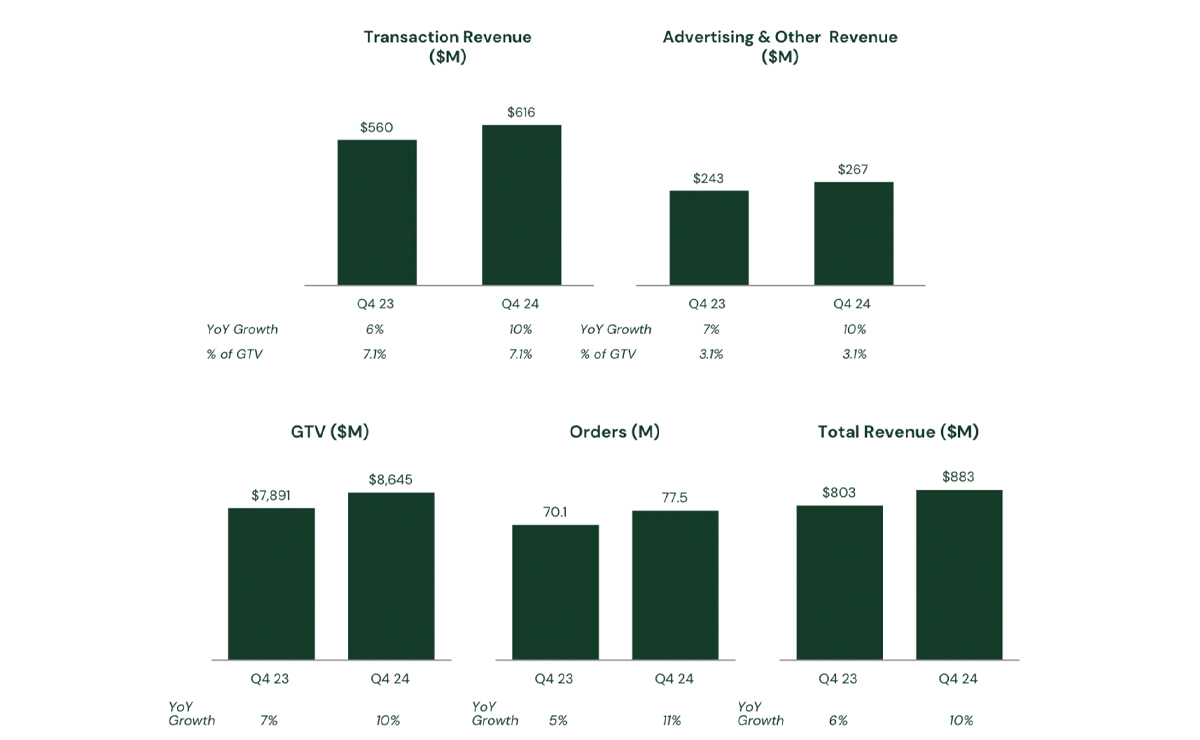

Let’s take a look at the top line. Instacart’s Q4 revenue jumped 10% year-over-year to $883 million, supported by an 11% year-over-year increase in orders. For the full year, revenue and order growth followed a similar pattern, up 11% and 9%, respectively, year-over-year.

That performance was supported primarily by revenue from transactions – up 11% to 2.4 billion during 2024 – rather than its ads arm, which grew 10% and contributed $958 million to the balance sheet.

The advertising arm has become a key focal point for innovation in the two years since Instacart became a publicly traded company, and CEO Fidji Simo defended those efforts despite slower-than-expected growth in the segment. She emphasized the results are a product of the macroeconomic environment, created by strained budgets across food and beverage, a factor other retail media networks are buffered from as most cater to the CPG industry at-large.

“This results in a virtuous cycle of growth, performance and scale,” she continued. “This momentum is fueled by our solid unit economics and critical advantages giving us a unique ability to capitalize on the massive opportunity in front of us in ways that our competitors simply can’t.”

Instacart currently has over 7,000 active brand partners, 1,800 retail banners and 600 enterprise storefronts on the platform. The platform continues to see its user base increase and brand partners roll out new innovations to keep users increasing basket sizes and ordering more frequently. In Q4, the grocery tech company dropped its minimum order size for $0 delivery fees from $35 to $10 for Instacart+ members.

“We’ve grown the overall number of people who use Instacart in the past year and drove quarterly users to order monthly and monthly users to order weekly at faster rates, year over year,” Simo said during a call with analysts. “In addition to growing order frequency, we also offer more value to our Instacart+ members who are growing faster than monthly users and remain our most loyal and engaged audience.”

Simo also emphasized the company’s efforts to support the grocery industry as the environment continues to tighten. By adding restaurants to its platform, Instacart has seen a “halo effect” on grocery over time as the additional use case creates “more stickiness” for the platform’s service.

Beyond its own business, Instacart is also working directly with retailers to steer pricing strategies and align rates on the platform with the price at-shelf in store, which it believes will support “affordability” of products across grocery. Most recently, Kroger introduced same-as-in-store pricing on items featured in its weekly ads and both Schnucks and Heritage Grocers Group moved to price parity chain wide and across all items.

“We also continue to encourage grocers to move to price parity with their stores, as we’ve seen that the ones that do have grown much faster on our platform,” Simo said.